Projected construction of a timber industry complex on the Sakhalin island, Russia, will have the capacity to process over 1.2 million m³ of raw material per year

The ECC (Eurasian Communication Centre) along with WhatWood consultant agency had been tasked by the government of the Sakhalin region to conduct a study of the timber industry’s possible development directions within the Sakhalin area. This article presents the main findings of the study.

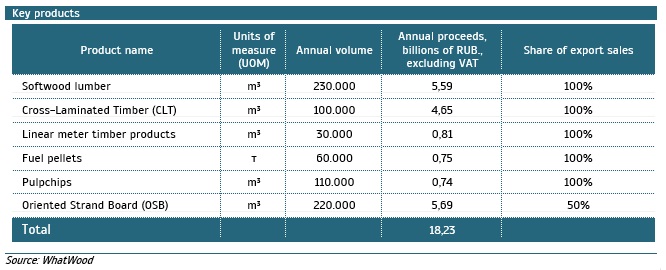

By the directive of the Sakhalin regional government, it is planned to construct one of the largest wood processing centers in all of Russia. The complex will be located in the central part of the island withing the Tymovskoye urban locality. The project will incorporate a diversified range of production, including softwood lumber, cross-laminated timber products, linear meter timber products, fuel pellets, fuel chips and oriented strand board products. The timber industry takes up a position in the top-10 list of measures for implementing the “Strategy-2035” plan in the region.

The economic feasibility of the timber industry construction within the Sakhalin region is apparent: availability of resources, proximity to major sales markets (China, Japan, Korea) and ready-made infrastructure.

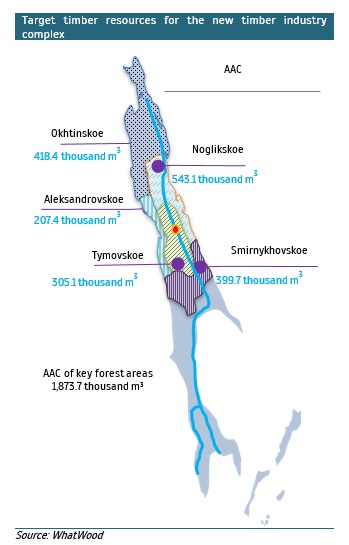

The target annual consumption of raw wood materials by the region’s timber industry is estimated be up to 1.2 million m³ per year. The species structure is mainly composed of conifers (77% softwood and 23% hardwood species). The annual allowable cut for the target forest districts (Okhtinskoe, Noglikskoe, Aleksandrovskoe, Tymovskoe, Smirnykhovskoe) adds up to 1.9 million m³ per year.

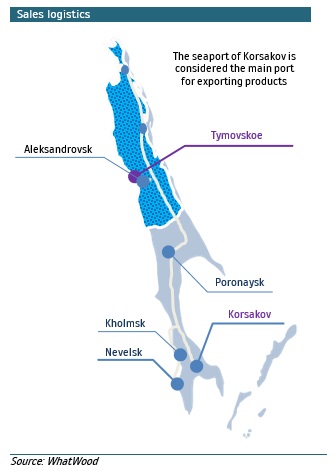

The production site location is selected in such a way as to minimize the hauling distance. The average transportation distance by timber trucks is 153 km.

The program of port modernization will improve the transport connectivity of Sakhalin.

The year-round seaport of Korsakov is regarded as the main export supply base. The area is also well positioned in terms of logistics for finished product distribution. The distance to the ports of Toyama – 645 km, Yokohama – 864 km, Shanghai – 1373 km, Busan – 939 km. The regional government is focusing on the development of port infrastructure and a state program for the “Development of transport infrastructure and road facilities” is in place.

In 2019, VEB.RF supported a project to modernize the port of Korsakov. It is planned to create a powerful logistics park on the basis of the sea port.

The creation of a multifunctional port will enable it to form a large hub for the transshipment of timber cargo, travelling via the route “Countries of the Asia-Pacific region – Russia – Europe”. Today, the maximum depths of the port reach 10.5 meters, when after reconstruction these parameters will increase to 14 meters. The work on lengthening the berths and deepening the waters will make it possible to receive large-capacity vessels. The turnover of goods after the modernization of the port will triple and reach 3 million tons per year.

In addition to this, the Ministry of Transport of the Russian Federation has published directives for the reconstruction and modernization of four large ports in the Far East, including the Sakhalin ports of Nevelsk and Kholmsk. The reconstruction will be carried out within the framework of “Logistics of International Trade” federal project. According to plans, construction work is scheduled to take place between the years 2021 and 2023.

The port of Nevelsk will be reopened as a permanent cargo and passenger checkpoint for crossing the state border of the Russian Federation. This is scheduled to happen after the construction work is completed between the years 2022 and 2023. After this reconstruction, the port’s capacity will reach over 6,000 transport vessels per year, taking into account seasonal terminals.

After the modernization process, the port of Kholmsk will increase its capacity to 1,500 vessels per. This number will include: 32 units of passenger ships per year or up to 1 unit per day, 1468 units of cargo ships per year or 4 units per day. The port reconstruction will take place in 2021-2022.

The timber industry complex is focused on complete integrated processing of timber materials

The project is focused on two aspects: traditional softwood lumber and the production of modern or developing types of wood products. Such products can include glued multilayer CLT plates and wood fuel pellets. This approach will ensure the stability of the project in the target markets. It will encompass processing of all types of industrial wood and recycling the entirety of the wood waste created during production.

Proximity to key consumption markets assures stable demand for products

The forest funds of Japan, South Korea and China are unable to supply the current or future demand of their internal markets in either short-term or long-term perspective. This market can only be fulfilled with lumber products by the means of import. As an example, the markets of Japan and China depend on import of softwood lumber by 40.1% and 48.5% respectively. Lumber manufacturers from Russia act as major suppliers, with the main production located in north-western Russia and Siberia. The capacity of these target markets (Japan, South Korea and China) is estimated at almost 100 million m3 of lumber consumption per year.

China has been the main driving factor of softwood lumber market growth. It has increased its consumption of lumber products by 2.8 times in the past 9 years, totaling to about 70 million m3 per year. Despite the insignificant short-term decline of demand in Japan and stagnation in South Korea, the general market for softwood lumber for the target countries has multiplied and reached a total of 87,4 million m3 per year. China’s explosive growth in consumption is leading to the increase of prices on lumber. This growth results in the surge of supply coming from Russian manufacturers, gradually squeezing out Canadian and U.S. suppliers.

CLT panels are in demand in Japan. Their consumption is fully subsidized. The goal of the Japanese government is to bring the consumption of these panels in housing and civil engineering to 500 thousand m ³ by 2025. The main import of CLT panels to Japan at the moment falls on remote Germany and Austria.

CLT panels are in high demand in Japan. Their usage is entirely subsidized by the Japanese government with the goal of achieving 500 thousand m3 of yearly panel consumption in housing and civil engineering construction by the year 2025. The main import of CLT panels in Japan is currently happening from remotely located Germany and Austria.

Russian suppliers are limited only in the Korean market. The main deliveries in the region are made from Vietnam, Malaysia and North America. The adopted state programs for the development of the fuel pellet market in Japan suggest an increase in consumption to 15 million tons by 2030, and the South Korean market to 6 million tons by 2021. With an increase in fuel pellet consumption in China, the regional market will be the largest in the world.

The fuel pellet markets of South Korea and Japan are constantly growing and are import dependent, while Russian suppliers only have a limited presence in the South Korean market. The main shipments to this region are taking place from Vietnam, Malaysia and North America. The newly adopted state program of incentivizing growth of the fuel pellet market in Japan is estimating a rise in consumption to 15 million tons per year by 2030, while the market in South Korea is estimated to grow to 6 million tons by 2021. With the added growth of fuel pellet consumption in China, this regional market is becoming the largest in the world.

Japanese and Chinese pulp and paper industries (PPI) gather chips from across the Asia-Pacific region and grow fast-growing trees on plantations in Australia for chip production. The largest fleet of chip hauling ships belongs to Japan. The decline of the global PPI did not affect China, which increased its pulp consumption by 4.7 times in the past 19 year. The regional market has multiplied, and its consumption is about 42.5 million tons, despite the decline of consumption in Japan.

Amid the export restrictions of round wood from Russian, the issue of supplying regional enterprises with raw wood material is becoming more and more critical. Further growth of pulp consumption is forecasted in China, including in-house produced material.

The Far Eastern Federal District market is characterized by a lack of building materials, which also leads to out of proportion housing prices and constrained volumes of construction. The entirety of the OSB is supplied to the Far Eastern Federal District by the European part of Russia. Transportation costs increase the cost of each board by almost 2 times. Regional domestic prices of OSB exceed export prices, what indicates to the “overheating” of the local structural panel market.

The project can be implemented in stages, with a gradual increase in production capacities and adaptation to local infrastructure. The construction period of the main project facilities is 1.2-2.0 years, excluding design and project approval stages.

The essential production complex, which ensures further development, is a sawmill production based on four-side chipping canter sawing technology and a center for processing waste into industrial chips and fuel pellets.

Project support by the regional authorities

Support measures for creating attractive conditions for investors include everything from priority in energy utility connection to the construction of railway lines from the place of manufacture to the renovated sea ports.

Another key aspect is the availability of regional tax benefits: income tax benefit and property tax befit. The preferential income tax rate is 2% from the moment of receiving the first profit to the payback of the project, but not more than 5 years and 10% for the next 5 years. The preferential property tax is 0% from the moment of placement on the balance sheet to the moment of payback, but not more than 5 years.

WhatWood Agency is ready to organize meetings of interested parties with the initiators of the investment project to discuss the details of cooperation.