WhatWood’s annual review: In 2013, Russian timber industry found its growth points

The last year has not brought any fundamentally new trends to the forest industry of Russia: companies tried to reduce the high cost of log procurement and production, also looking for new points of growth. Eventually export demand for sawn timber and wood pellets played the role of growth point, as said in the third annual review by WhatWood, “Russian forest industry in 2013“.

An undoubtedly new phenomenon in 2013 was only that the problems of the forest complex came out of the narrow industry status and became the subject of discussion at the highest state level. Session of State Council dedicated to the problems of the forest industry set a direction in the legislative activity of the state structures. Often this activity was chaotic and caused mass criticism of the companies and environmentalists, however, the government at least has found new people – the younger generation of specialists, who were more willing to cover the work of government agencies, attended industry conferences and listened to the opinion of experienced timber manufacturers and scientists.

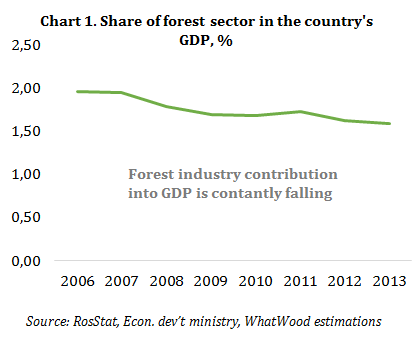

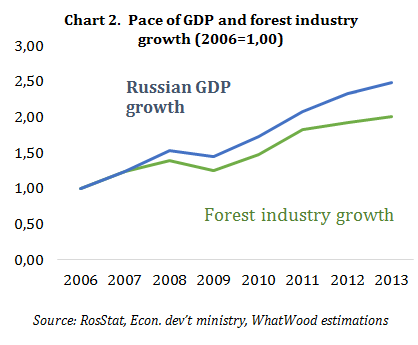

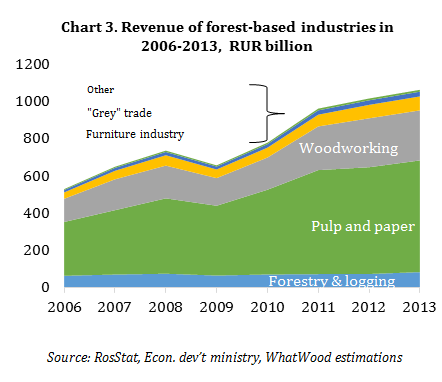

The volume of investments in the fixed capital of enterprises of the forest complex in 2013 decreased by 39% to 88.7 billion roubles, while consolidated revenues from sales of forest products increased by 5% to 951 billion roubles. The contribution of the forestry complex in Russia’s GDP also decreased by 0.03 percentage point to 1.59%: growth rate of revenues in the forest complex lags behind the total Russian GDP growth (see Charts 1, 2, 3). That said, all sectors of forest industry showed positive dynamics of revenue. The most dynamic was forestry and logging industry, fuelled by strong demand for roundwood from European buyers. The number of illegal seasonal sawmills declined, which also had a positive effect on the forestry. The pulp and paper industry, one of the most capital-intensive, reduced significantly its share, while the biofuel and biotechnology sector, in contrast, has reached a new stage of development and brought growth hopes for the forest complex.

Favourable situation on foreign markets helped extremely Russian timber merchants last year. China accounted for about 40% of the revenues of enterprises, European countries – for 35%. This trend may continue in 2014. China is now able to take the entire volume of production of sawn timber in Russia, Finland is still ready to buy deciduous pulpwood from the Northwest, and the demand for Russian birch plywood has not diminished in the United States and Europe by far. Given the projected reduction of prices for Russian lumber in Japan after the increase of the consumption tax in this country and still possible economic sanctions by Europe and North America, it can be expected that China will remain the main export market and will help Russian forestry, consuming its products at reasonable prices.

What is annual analytic study “Russian forest industry”:

– Detailed review of Russian forest-based industries. Major trends on the domestic market and overview of key export sales markets for Russian wood products.

– Overview of Russian economy: GDP, investments, construction and wooden housing, industrial production.

– Forest policy: legal changes in the forest-related laws of Russia.

– Forestry: review of the sector.

– Logging: volumes in terms of Russian regions, exports, sawlog and pulpwood monthly prices, special feature “Pulpwood trade balance and logging cost structure in the North-West Russia”.

– Woodworking: production (including Top-100 Russian sawn timber producers), investment projects, exports/imports of lumber and wood-based panels (plywood, chipboard, fibreboard, MDF, OSB), major trends on the key markets (Europe, Middle East, China, Japan), base prices for export deliveries.

– Pulp & paper: production of wood pulp, exports/imports of softwood sulphate bleached and unbleached pulp, of hardwood sulphate unbleached pulp. Paper and board exports/imports.

– Bioenergy: review of the wood pellet market (Russia, Europe, East Asia), exports/imports, investment projects, base and statistic average prices of pellet exports.

– Free additional publications: Top-100 forest industry companies in Russia and Summing-up price review for 2013.

The review has 111 pages (PDF format), 124 charts, 60 tables, and 10 maps.

To order the annual review, please write a request to zakaz@whatwood.ru or visit product page.