Russian Forest Industry Review in 2022-2023: a quarterly analytical review

Analysts from the WhatWood agency prepared the quarterly analytical Russian Forest Industry Review in 2022-2023. This is a completely new product that includes a detailed analysis of the condition of Russian timber industry segments and its key trends. The review also tracks the changes of key industry performance indicators (the trends of output, consumption, import, export, and prices by regions, enterprises, and product specifications) and contains comments of analysts and market players on the performance in each calendar quarter of the year.

Following requests to receive market data more quickly under the rapidly changing circumstances, we intentionally stopped making annual reports by various timber industry segments this year, so that our clients could receive analytical and statistical information across all segments of the Russian timber industry more promptly within a single review (4 issues per year, based on each quarter’s performance).

Russian timber industry performance in 2022

This has been the third consecutive year when we call the past year “extraordinary” as we summarize the timber industry performance in Russia and worldwide. The extraordinary year 2020 witnessed major disruptions in operation of enterprises and transportation because of ubiquitous lockdowns and restrictions on operation imposed by governments of many countries, up to complete shutdowns due to the spread of COVID-19. During the most stringent restrictive measures, in April-May 2020, some Russian timber enterprises were forced to idle for 1.5-2 months; in H2 2020, a budding growth of demand compensated for the slump in H1 2020. As a result, the performance of the Russian timber industry even improved by 10% YoY in 2020 (by revenue).

After a forced decline of output and consumption of timber products in 2020, a full-fledged recovery growth began in the year 2021 due to a boom in private consumption, a growing housing development sector, and, as a consequence, an extraordinary price surge. As a result, the year 2021 was the most successful in the contemporary history in terms of financial performance of the Russian timber industry. The revenue of timber enterprises soared by 32% YoY, up to 2.8 trillion rubles; their net profit, by 3 times, up to 460 billion rubles, and the timber industry’s contribution in the national GDP reached 2%.

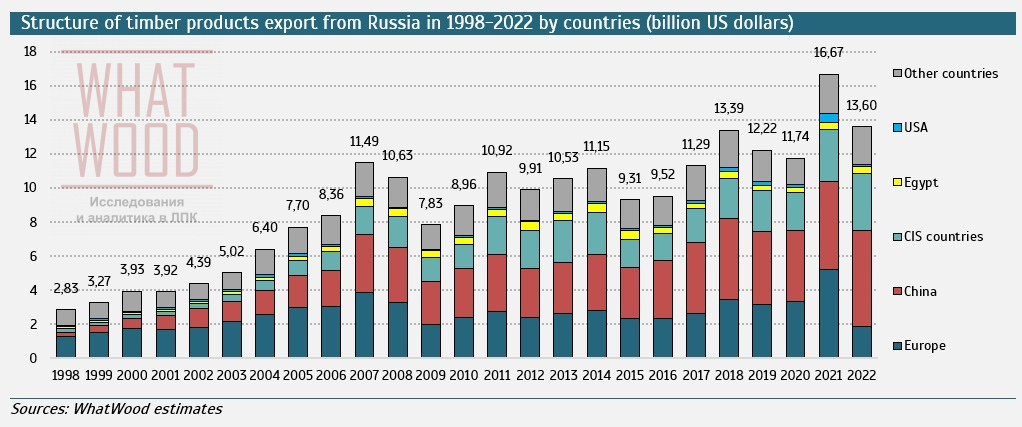

In 2020-2021, the performance of both global and Russian timber industry could be considered extraordinary, but the year 2022 was extraordinary for Russia alone. In 2022, the Russian timber industry had to grapple with the unprecedented pressure of sanctions, the complete closure of traditional European markets for the export of finished products made in Russia, higher transportation costs, the restructuring logistics market, many western partners’ leaving the Russian market, and an extremely low currency exchange rate. All this happened in the context of a rebound — in both global and domestic markets — of those prices for timber products that had reached their peak back in 2021, and amid the brewing global economic recession. In 2022, the performance of the Russian timber industry declined by 10% YoY (by revenue), although some areas, such as the plywood sector, dropped by over 30%. The general decline in the Russian timber industry’s performance is obvious but not catastrophic. It is, however, very perceptible compared to the ultra-high performance of 2021.

The Russian Government is trying to develop at least some support measures that would allow timber enterprises to adapt to new economic and market circumstances. Meanwhile, reimbursement of costs incurred through cargos’ export transportation remains the key support measure most eagerly sought by timber enterprises. In February 2023, the maximum amount of the subsidy for products’ export transportation was increased from 300 million to 500 million rubles. The upper limit of the reimbursement will be temporarily increased to 100% for timber enterprises in case of shipping products via northwestern ports of the Russian Federation.

The common theme of the first issue of the quarterly analytical Russian Forest Industry Review in 2022-2023 is the sanctions that fundamentally affected the operation of Russian timber enterprises.

In early 2022, we identified the four major triggers that could keep the Russian timber industry operable: a weak ruble, growing prices of timber products in the global market; capability to receive payments from abroad; and a reduction of logistics rates and finding new transportation routes for product delivery. It has now become obvious that companies capable of finding a way to deliver their products to the foreign market with minimum transportation costs will remain competitive in the market. With rare exceptions, the demand and need for timber products originating in Russia remain mostly high in the global market. Even European partners are ready to buy Russian products via third parties and new hubs in some cases.

Although we forecast a further decline of most performance indicators of the Russian and global timber industry in 2023, we expect the rates of this decline to slow down compared to 2022. The key problems and issues that timber enterprises will have to solve concern transportation and logistics.

WhatWood team, March 2023.

—

The quarterly analytical Russian Forest Industry Review in 2022-2023 includes:

– Quarterly updated forecast of the development of key indicators.

If you have any questions about the review, please call +7 985 939 85 52 or email zakaz@whatwood.ru